Join my email list to learn how I did it...

(Expect almost daily emails stuffed with actionable insights on how to buy your first property)

The Book I Found In A Dumpster That Made Me $80,000...

There I was, rifling through one of probably 40 different dumpsters.

I'd already made my rounds at the dump that day, looking in this bin and that.

Sure, there were a few decent finds, but this dumpster I was picking around in...

It was about to change my life forever.

I had just hopped in (yes, my whole self inside the dumpster) and was digging through what seemed to be some old office supplies...

It was almost as if a secretary had tossed everything that was in her office right into this bin.

Then I saw it: "YOU CAN CHOOSE TO BE RICH!" by Robert Kiyosaki.

It was a handsome package, containing a couple workbooks and a few cd's. The title intrigued me.

I grabbed it and took it home, thinking to myself: "Who is this Robert Kiyosaki guy?"

After some brief research some days later, I realized that the name sounded familiar because I'd seen it before.

At the age of 13, my parents had given me a list of impactful books to read to expand my mind, heart, and spirit.

Rich Dad, Poor Dad was on the list.

Upon connecting the dots, I got my hands on "Rich Dad, Poor Dad," "Cashflow Quadrant" and any other Kiyosaki materials that were available online or in used bookstores, and started devouring them like a ferocious animal.

Everything.

These ideas... These concepts... These simple, yet paradigm shifting diagrams... It was like drinking from a gushing fire hydrant–

of fire.

My pencil sketched 5-year plans were going up in flames. You know, the plans like:

Become an EMT firefighter and pay my way through college...

Make up some hodgepodge interdisciplinary degree that my school didn't even offer as a program (something foreign language oriented) and try to graduate with zero debt...

Become some sort of minister (well, still did that in a manner of speaking 😉)...

All of it was disentigrating before my eyes because... Well, no one had ever told me anything like this before!

Assets, liabilities, cash flow, thinking like the rich, not working for money...

I'd never considered "real estate" or "asset based income" as viable pursuits because I'd never even heard of them.

My high school classes were fresh out of such ground breaking content.

All of a sudden, I knew exactly what I wanted to do:

Buy my first property, and stuff my balance sheet full of cash flowing assets like there's no tomorrow–just like Rich Dad.

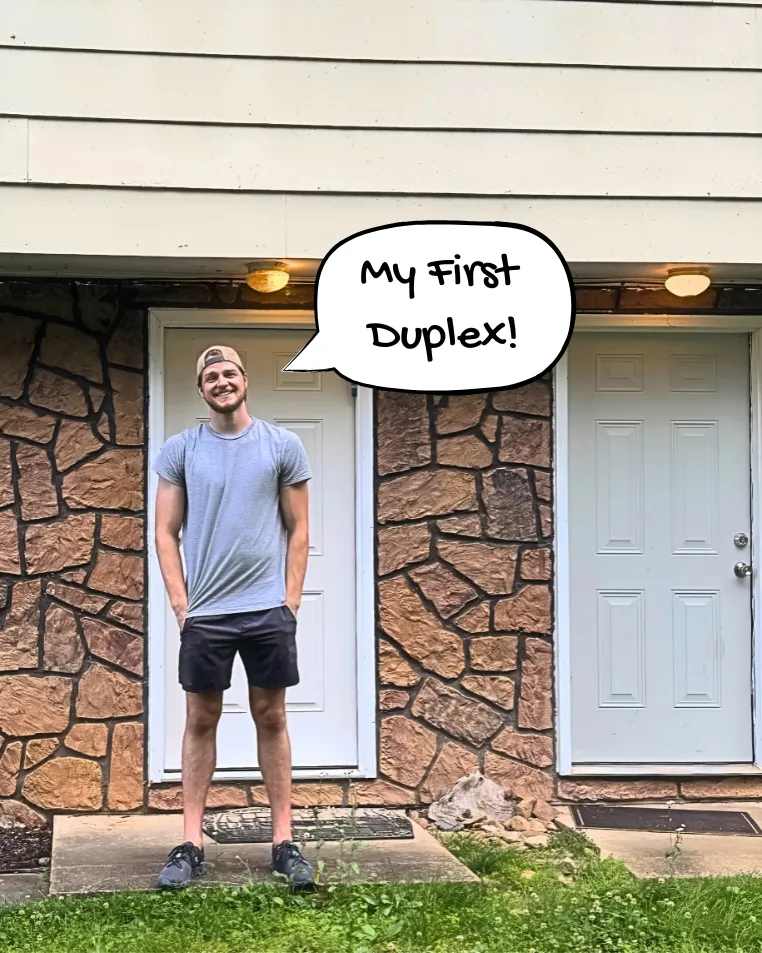

Fast forward to age 21 - I bought my first duplex with only $3,945.09 out of pocket.

That's not a typo.

Less than four grand to buy my first property.

Most people think you need a massive down payment and perfect credit to accomplish this. They're wrong.

I'm living proof that anyone can do this with the right strategy.

That's why I created EasyFirstProperty.com–to show you how to get your hands on your first property.

I break everything down into simple steps that actually work. No BS, No fluff.

Want to know how I did it?

I'm sharing the strategies I used in my almost daily newsletter.

>>> Click Here To Join My Email List

Real estate changed my life.

Now I help others change their lives by buying their first property.

This is who I am. From dumpster diver to property investor to your guide.

Let me show you how to change your life with real estate.

-Jonathan

My Latest Articles

How To Build Amazing Credit

The Unspoken Language of Lenders

Here’s the thing: lenders don’t know you. They don’t know your work ethic, your dreams, or the hours you’ve put in to save for a down payment. They know your credit score. That’s the lens through which they see you. To them, your credit score is a narrative—a shorthand way of understanding how you’ve handled financial commitments in the past and whether you’re likely to hold up your end of the deal in the future.

Think of it like a first impression at a job interview. A high credit score says, “I’m reliable, I’ve got this.” A low score raises questions: “Will you make payments on time? Are you stretched too thin? Will you follow through?” It’s not personal, but it is pivotal. And when it comes to mortgages, the stakes are high.

The Math Behind the Story

Your credit score is built on five pillars, and each one plays a role in determining whether you’re ready to take on the responsibility of a mortgage.

1. Payment History (35%)

Imagine you’re lending money to a friend. Would you want to know if they’ve paid back loans before? That’s payment history in a nutshell. It’s the biggest piece of the pie because it speaks directly to your reliability. Late payments, defaults, or collections are like red flags flapping in the wind. On the other hand, a history of on-time payments is a green light.

For mortgage lenders, this is the ultimate trust metric. If you’ve missed a few credit card payments in the past, now’s the time to lock in a streak of consistency. Automate payments, set reminders—do whatever you need to do to keep that history spotless moving forward.

2. Credit Utilization (30%)

Your credit utilization ratio measures how much of your available credit you’re using. Think of it like a gas gauge for your financial health. If you’re using 90% of your available credit, you’re running on fumes, and lenders see that as risky. Aim to keep this number below 30%, though under 10% is even better.

But this isn’t just about optics. Your credit utilization also feeds into your debt-to-income ratio (DTI), which lenders scrutinize when you apply for a mortgage. A high DTI, even with a decent credit score, can throw a wrench in the approval process. If you’ve got balances creeping up, chip away at them now. It’s a small effort that can have a big payoff. More insights on work history and income coming to you shortly; stay tuned🔥!

3. Length of Credit History (15%)

This is where time works in your favor. The longer your credit accounts have been open, the more data lenders have to assess your habits. A well-managed account that’s been around for a decade carries more weight than a shiny new credit card.

If you’re new to credit, don’t stress. Start building now. Get a secured card, become an authorized user on someone else’s account, or take out a small, manageable loan. And whatever you do, don’t close your oldest accounts—they’re part of your financial legacy.

4. Credit Mix (10%)

Mortgages, credit cards, student loans, car loans—having a mix of credit types shows lenders you can juggle different financial obligations. It’s not the most significant factor, but it helps round out your profile. Just don’t fall into the trap of opening new accounts just to diversify. Credit mix matters, but not enough to risk taking on unnecessary debt.

5. New Credit (10%)

Every time you apply for credit, a hard inquiry appears on your report, and your score takes a small hit. Open too many new accounts in a short period, and lenders may see you as financially unstable. If you’re preparing to buy a home, pump the brakes on new credit applications. Focus on stability and maintaining what you’ve already built.

(Note: Often times your lender will review your credit report to check for inquiries, and likely will ask for explanations for each inquiry if it is within a certain time frame from your application. they will have to create what is called a "credit explanation letter" or a "CEL" and present that to their underwriter during your approval process. It is best to wait a couple of months after getting any other credit before applying for a mortgage.)

If I hadn't started early:

If I hadn't started building credit YEARS in advance, I would have never been able to do my first real estate deal.

Why?

Because in order to get that first deal, I had to buy a house that needed work. As we all know, there ain't no such thing as a free lunch.

I would have to pay to get that property renovated.

Luckily, I started building credit when i was 18, and I had large credit lines available to pay for property repairs.

But I didn't start with a $20k business credit card that did report to my personal credit... (yeah, for real. i had $10k on a 0% APR business credit card during the entire time i was qualifying and buying that first house, and the mortgage lender had no idea about it. stay tuned to learn how the heck I pulled that off; more insights to come 🔥), I started with a great card, and a limit less than $2000.

Credit Card Recommendation

The card I started with is none other than the CapitalOne QuicksilverOne.

If you have a little bit of credit established and are looking for a great card, I recommend the QuicksilverOne. This card gives you UNLIMITED 1.5% Cash Back. This card is easier to qualify for than Chase cards, in my opinion. And you can See if you're Pre-approved before applying!

This is a great place to start. Let me know if you got approved :)

Connecting the Dots to a Mortgage

So, why does all this matter when it comes to buying a house? Because your credit score is one of the main things considered by lenders. When it comes to buying a property, it’s not just about whether you can get a loan—it’s about what kind of loan you’ll qualify for. Believe me, you want the best loan you can possibly get. Higher interest loans eat into your cash flow from your properties.

A high credit score opens doors. It gets you lower interest rates, which means lower monthly payments and tens of thousands of dollars saved over the life of the loan. It also gives you leverage: better terms, more options, and a smoother approval process. On the flip side, a low score can limit your choices—or shut the door entirely.

For example, when I bought and renovated my first home, my credit score was a crucial piece of the puzzle. It allowed me to secure low-interest financing for the purchase and leverage credit lines for renovations. That didn’t happen by accident—it was the result of years of intentional credit building and financial planning.

How to Strengthen Your Score Now

Here’s your roadmap for mortgage readiness:

Pull Your Credit Report:Knowledge is power. Review your report for errors, and dispute anything that doesn’t look right. You can access this 1 time per year without an impact on your score onthis website.

Prioritize Payments:If you do nothing else, pay every bill on time. This alone can make a massive difference.

Reduce Utilization:Pay down credit card balances, and aim to keep utilization below 30%.

Avoid New Credit:Hold off on new applications until after you’ve closed on your home.

Talk to a Lender Early:Sit down with a lender to understand the specific score and DTI requirements for the loan you want.

The Bigger Picture

Here’s what I love about the credit score conversation: it’s not just about numbers. It’s about how those numbers translate into opportunity. It’s about putting yourself in the best possible position to say “yes” when the right property comes along. And most importantly, it’s about taking ownership of your financial story.

Building a strong credit profile doesn’t happen overnight, but every step you take today is a step toward the life you’re creating. If you’ve been on my email list for any amount of time, you know this journey isn’t about quick wins—it’s about steady, intentional progress. Your credit score is one more piece of that puzzle.

So, keep grinding. Keep building. And remember: every time you make a payment on time, every balance you pay down, every smart decision you make—it’s all part of a much bigger plan, and that plan is leading you to the keys to your first (or next) property.

Keep watching and reading.

Talk soon,

-Jonathan

Contact Me!

Copyright 2025. All Right are Reserved. Easy First Property

Privacy Policy | Terms & Conditions